Ipsos Poll: Canadians Are Less Than $200 From Hardship, Implications For The Economy And Strategies To Tackle Debt, Explained

The recent Ipsos poll conducted on behalf of MNP Ltd. paints a worrisome picture of the financial health of Canadian households. With more than half of Canadians indicating that they are only $200 or less away from not being able to make ends meet, the implications for the economy are far-reaching. This article delves into

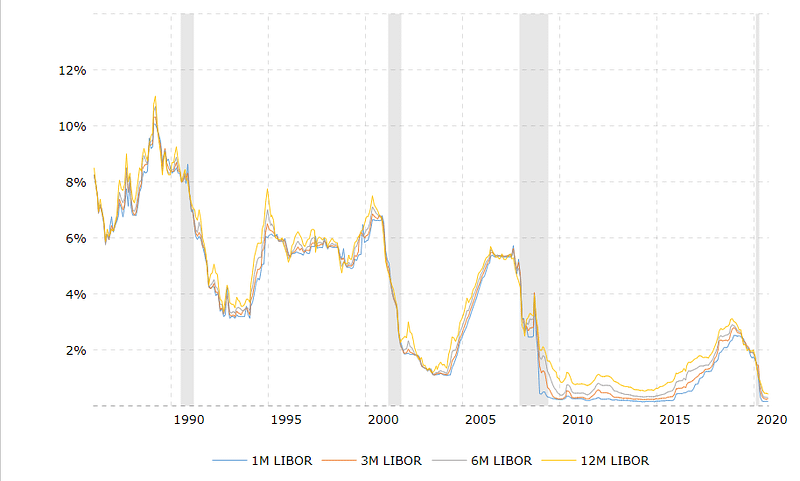

Unveiling The Historical Norm: Preparing For A Return To Higher Interest Rates In Canada

Canada experienced an unprecedented period of historically low interest rates from 2009 to 2020. However, as we move into an era of rate hikes after rate hikes, it is important to recognize that this low interest rate environment was actually an outlier and to prepare for the future. This analysis aims to shed light on

Navigating Canada’s Rising Interest Rates: 9 Strategies to Eliminate Debt

In the wake of the Bank of Canada’s recent decision to raise interest rates to 4.75%, Canadians find themselves facing a new, harsher financial reality. With higher costs associated with borrowing money, it becomes very important for individuals to prioritize debt reduction strategies. The following article will provide you with actionable tips and insights on

7 Tips To Rebuild Your Credit In Canada

As a Canadian, you know that your credit score is an incredibly important aspect of your financial health. It can affect everything from your ability to get a loan or mortgage, to the interest rates you’ll pay on those loans. If you have a low credit score, it can feel like you’re stuck in a

Should You Pay Your Debts Or Invest Money?

It’s a common question many people face: should I pay off my debt or invest my money? The answer isn’t always straightforward, and it ultimately depends on your individual financial situation. In this blog post, we’ll explore the pros and cons of both paying off debt and investing. We will also provide some guidance on

4 Easy Tips To Help You Live Within Your Means

You may be living beyond your means if you are using credit cards to pay for regular expenses, if you’re unable to save money each month, or if you’re constantly borrowing money from friends or family. If any of these apply to you, there are a few things you can improve short term. To be